Orthopedic Medical Device Market Booms: Net Profits of 6 Listed Companies Surge Collectively in First Half of the Year!

According to Smart Medical Devices Network, data shows that the global orthopedic medical device market grew from $35.2 billion in 2016 to $46 billion in 2023. Driven by factors such as global population aging, increased incidence of orthopedic diseases, and continuous development of emerging medical technologies, the orthopedic market is expected to continue growing.

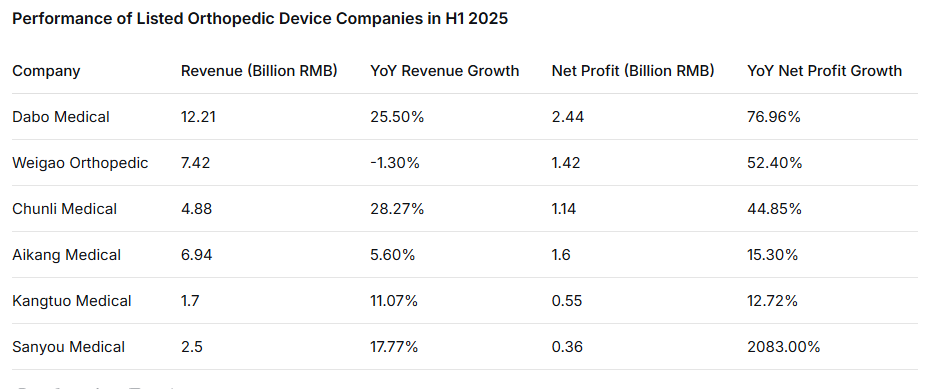

Recently, Smart Medical Devices Network compiled the first-half performance reports of several listed orthopedic companies, including Dabo Medical, Weigao Orthopedic, Chunli Medical, Aikang Medical, Kangtuo Medical, and Sanyou Medical. Among them, the net profit year-on-year growth rates for Dabo Medical, Weigao Orthopedic, and Chunli Medical in the first half were as high as 76.96%, 52.4%, and 44.85% respectively, with Sanyou Medical reaching an astounding 2083.64%.

Overall, the growth factors are twofold: First, the market is experiencing rapid growth. Compared to overseas markets, the domestic orthopedic medical device market still has significant room for development. Second, the negative impact of volume-based procurement has passed, and most companies have largely adjusted. With the expected rapid market development in the future, it is foreseeable that the performance of these companies will further improve.

01 Dabo Medical: Net Profit Increased by 76.96% YoY

According to Dabo Medical's H1 2025 results, the company achieved revenue of 1.21 billion RMB, a year-on-year increase of 25.55%. The revenue growth was attributed to further increased market share both domestically and internationally, leading to corresponding increases in domestic and export sales. Meanwhile, the company's net profit reached 244 million RMB, a year-on-year increase of 76.96%.

Information shows that Dabo Medical's main business is the production, R&D, and sales of high-value medical consumables. Its main products include orthopedic trauma implant consumables, spinal implant consumables, joint implant consumables, sports medicine and neurosurgical implant consumables, minimally invasive surgical consumables, and dental implant consumables, among others.

Trauma Implant Consumables: Primarily used for pathological/traumatic fracture repair or orthopedic needs in adults and children involving the upper/lower limbs, pelvis, hip, hands, and ankles. Products include intramedullary nails, metal bone plates, bone pins, screws and other internal fixation systems, and external fixators.

Spinal Implant Consumables: Primarily used for surgical treatment of various spinal disorders caused by trauma, degeneration, deformity, or other pathological reasons. Products include pedicle screw systems, spinal plate systems, interbody fusion devices, vertebroplasty series, and various spinal internal fixation devices.

Neurosurgical Implant Consumables: Primarily used for cranial bone fixation or defect repair, maxillofacial fracture or orthognathic fixation, etc. Products include maxillofacial titanium mesh, maxillofacial bone plates, cranial titanium mesh, cranial bone plates and screws, and other internal fixation systems.

Joint Implant Consumables: Primarily used for treating joint diseases like osteoarthritis, rheumatoid arthritis, and osteonecrosis of the femoral head. Products include artificial hip joint systems and artificial knee joint systems.

Sports Medicine Implant Consumables: Used for ligament injury repair/reconstruction and orthopedic internal fixation. Products include non-absorbable suture anchors, toggle plates, etc.

Dental Implant Consumables: Primarily used for tooth loss restoration. Products include dental implant systems, etc.

Minimally Invasive Surgical Products: Mainly used for establishing instrument access and providing devices for minimally invasive surgeries. Products include disposable laparoscopic trocar series, disposable single-port multi-channel laparoscopic trocar series, disposable minimally invasive fascial closure device series, etc.

02 Weigao Orthopedic: Net Profit Increased by 52.4% YoY

In the first half of the year, Weigao Orthopedic reported revenue of 741 million RMB, a slight decrease of 1.3% year-on-year. However, net profit attributable to shareholders was 142 million RMB, a significant increase of 52.4% YoY. After excluding non-recurring gains and losses, net profit was 136 million RMB, also up 52.0% YoY. In the second quarter alone, revenue was 451 million RMB, up 11.9% YoY; net profit attributable to shareholders was 90.17 million RMB, up 54.9% YoY; and adjusted net profit was 86.73 million RMB, up 58.3% YoY.

The company's products comprehensively cover spine, trauma, joints, sports medicine, bone repair materials, tissue repair, and orthopedic surgical instruments.

Spine Products: Mainly consist of spinal implant devices, vertebroplasty systems, and spinal minimally invasive products, under the four brands "Weigao Orthopedics," "Weigao Yahua," "Weigoa Haixing," and "Quantum Medical." These products provide precise and effective treatment solutions for spinal deformities, degenerative diseases, spinal fractures, tumors, etc.

Trauma Products: Mainly include locking plate systems, intramedullary nail systems, cannulated screw systems, and external fixation systems, under the three brands "Weigao Orthopedics," "Jianlibangde," and "Weigao Haixing." Designed for fractures caused by trauma, they enable precise reduction, stable fixation, and long-term maintenance for various complex fractures.

Joint Products: Cover hip and knee prosthesis systems, mainly under the "Weigao Haixing" and "Weigao Yahua" brands. These systems enable effective functional reconstruction for joint disorders caused by periprosthetic fractures, bone tumors, etc.

Reportedly, Weigao Orthopedic adjusted its sales model for joint products from a distribution model to a dealership model, which led to the decrease in revenue. However, the report noted a significant decrease in the sales expense ratio, attributed to optimizations in marketing structure, channel integration, and market expense management.

Regarding products, the company's main products span spine, trauma, joints, and other areas, with steady market demand growth. The company actively promotes the sales of non-tender products to increase market share. Furthermore, the report mentions continuous R&D investment, particularly innovation in spinal minimally invasive surgery and sports medicine. Overall, despite short-term impacts from the sales model change, the company maintains a positive long-term development and market layout trend.

03 Chunli Medical: Net Profit Increased by 44.85% YoY

Chunli Medical's H1 2025 report shows the company achieved revenue of 488 million RMB in the first half, a year-on-year increase of 28.27%. Net profit attributable to shareholders was 114 million RMB, up 44.85% YoY. After excluding non-recurring gains and losses, net profit was 106 million RMB, up 61.09% YoY.

The company's main products include joints, spine, sports medicine, trauma, orthopedic surgical robots, and orthopedic surgical instruments. Joint prosthesis products cover hip, knee, shoulder, elbow, and small joints. Spinal implant products comprise a full range of spinal internal fixation systems. Sports medicine products include suture anchors, interference screws, toggle plates, staple screws, surgical sutures, etc. Trauma products include bone plates, intramedullary nails, external fixators, metal bone pins, etc. Orthopedic surgical instruments include retractors, periosteal elevators, bone holders, bone drills, bone mallets, bone rasps, osteotomes, etc. Orthopedic surgical robots primarily consist of navigation systems for hip replacement, knee replacement, and unicompartmental knee replacement.

In the domestic high-value orthopedic implant consumables sector, the company consistently maintains a leading position. On one hand, it continues to drive innovation in its core joint business, committed to creating a diverse range of products suited to the bone structure and needs of the Chinese population, solidifying its leading position in the domestic joint implant market.

On the other hand, the company actively expands and improves its product lines within orthopedics. It not only covers orthopedic robots, spine, sports medicine, and trauma products but has also made strategic layouts in dental, PRP products, medical aesthetics, and orthopedic power tools.

Simultaneously, the company pays close attention to the development trends of related new technologies in the industry, especially cutting-edge dynamics in new materials, conducting forward-looking research and layout to prepare fully for sustainable future development. In market expansion, the company adopts a dual approach: consolidating its leading domestic position while simultaneously strengthening its international business team, increasing investment in international market promotion, and fully exploring global opportunities.

04 Sanyou Medical: Net Profit Increased by 2083.64% YoY

Sanyou Medical released its 2025 semi-annual report. The report shows that the company achieved revenue of 250 million RMB in the first half, a year-on-year increase of 17.77%. Net profit attributable to shareholders was 36.6008 million RMB, a substantial year-on-year increase of 2083.64%. Profit after excluding non-recurring items also successfully turned profitable, reaching 26.0241 million RMB. The performance significantly exceeded expectations, demonstrating strong growth momentum.

Sanyou Medical stated: "Currently, the industry as a whole is still constrained by the National Volume-Based Procurement policy and related healthcare policies. Under the influence of these policies, industry concentration has increased. During the process of product innovation, import substitution, and the implementation of National Volume-Based Procurement, some companies have exited the Chinese market, and Sanyou Medical's share in the domestic implant market has increased. Currently, national policies strongly support innovation in high-end medical devices, which is favorable news for companies like Sanyou that emphasize independent R&D and innovation and possess rich experience and technological reserves in product/therapy innovation."

Simultaneously, Sanyou Medical stated that in the volume-based procurement environment, facing a more complex and severe operating environment and industry competition, it will ensure production capacity supply, maintain normal operating turnover, continue to insist on therapy innovation, adopt more flexible and effective methods for domestic and international market expansion, build upon its existing product lines—spine, trauma, and ultrasonic power systems—utilize its operational network to promote sales of existing operational products like capsules and bone cement, continuously advance strategic planning and business layout in related orthopedic fields such as sports medicine, new orthopedic materials, AI, and surgical robots, and further enhance its R&D strength and core competitiveness. Additionally, Sanyou Medical will strengthen lean production management, improve production efficiency and asset utilization, reduce production costs, enhance management efficiency, and continuously lower its comprehensive costs.

05 Aikang Medical: Net Profit Increased by 15.3% YoY

In the first half of the year, Aikang Medical achieved revenue of approximately 694.2 million RMB, an increase of approximately 5.6% compared to H1 2024. Net profit was approximately 160.6 million RMB, an increase of approximately 15.3% YoY. In H1 2025, driven by the volume-based procurement policy, import substitution accelerated further, leading to sustained growth in demand for the company's products used in surgeries, and sales of products included in the procurement volume achieved further growth.

In 2025, under the dual drivers of active national policy guidance and continuous market vitality release, China's medical industry is accelerating its transformation towards high-quality development. Aikang Medical accurately seized policy opportunities, aligned national strategies with corporate development goals, and further strengthened its position in the first tier of China's orthopedic industry.

In H1 2025, following the National Healthcare Security Administration's announcement of the "Follow-up Procurement Winning Results for Expired Artificial Joint Volume-Based Procurement Agreements" last year, the follow-up procurement policy for artificial joints was fully implemented across all provinces, accelerating import substitution and bringing new market and customer opportunities for the company. Leveraging its excellent product reputation and strong product capabilities, Aikang Medical further accelerated import substitution, achieving extensive coverage of national and provincial key hospitals.

In H1 2025, with the completion of the new industrial park, the group established a digital orthopedic interaction platform and experience center, realizing integrated services for the full-process digital orthopedic solution. Furthermore, it integrated physical displays with virtual simulation technology, enabling multiple functions such as product display, physician training, patient education, and clinical verification, creating a doctor-engineering interaction platform and a window for showcasing innovation achievements.

In H1 2025, the company's K3 intelligent surgical robot received approval from the NMPA for market launch. The company continuously improved the construction of the iCOS digital orthopedic customized product and service platform, completed the closed-loop of the orthopedic digital ecosystem, continuously expanded market share, and strengthened its leading position in the orthopedic field.

The iCOS digital orthopedic platform builds a full-process solution covering "preoperative planning - intraoperative navigation - postoperative monitoring," allowing doctors to perform 3D customized preoperative planning, achieve precise connection with robotic/navigation systems intraoperatively, and provide rehabilitation optimization tools postoperatively. Combined with the "standard - complex - customized" implant product line, it innovatively launched an integrated, full-chain solution of "preoperative planning + intraoperative navigation/robotic system + implants." This realizes the transition from single product sales to overall solution value delivery, promoting the industry's upgrade towards a value-based medical model.

06 Kangtuo Medical: Net Profit Increased by 12.72% YoY

Kangtuo Medical disclosed its 2025 semi-annual report. In the first half, the company achieved revenue of 170 million RMB, a year-on-year increase of 11.07%; net profit attributable to shareholders was 54.9986 million RMB, an increase of 12.72% YoY; and profit after excluding non-recurring gains and losses was 50.3874 million RMB, an increase of 25.02% YoY.

Kangtuo Medical is a high-tech enterprise focused on the R&D, production, and sales of Class III implantable medical devices. Its main products are used in neurosurgical cranial repair/fixation, cardiothoracic surgical sternal fixation, maxillofacial repair, and the dental field. As of the first half, the company holds 20 Class III implantable medical device registration certificates, involving several pioneering products in细分 segments. It holds the largest market share in China for PEEK cranial repair and fixation products and is the only domestic enterprise capable of providing a full PEEK solution for neurosurgical cranial repair/fixation tailored to patient needs.

In the first half, leveraging strong technical capabilities and product innovation, Kangtuo Medical maintained steady growth in its neurosurgical cranial repair/fixation business. The company holds the largest domestic market share for PEEK cranial repair/fixation products and is the only domestic enterprise capable of providing a full PEEK solution for neurosurgical cranial repair/fixation around patient needs.

As a leading enterprise in the neurosurgical implant device field, the company relies on its core technological积累 in PEEK materials and its comprehensive product matrix advantages to accurately grasp market dynamics and continuously provide personalized diagnosis and treatment solutions for patients.

In regional volume-based procurement for neurosurgical medical consumables, the company's PEEK cranial repair/fixation systems and traditional titanium products both won bids, with its market share continuing to lead the industry, further strengthening its benchmark position in the细分 segment of neurosurgical cranial repair/fixation.

With the deepening implementation of regional volume-based procurement policies and the steady increase in the clinical application proportion of innovative PEEK materials, the company is leveraging its technological iteration advantages to accelerate the replacement process of high-end products for traditional titanium materials. Based on its forward-looking layout in PEEK material application R&D, production processes, and clinical solutions, the company is expected to continuously expand its leading advantage in subsequent market competition, driving growth in both business scale and profitability.

In the first half, the industry influence of the company's neurosurgical cranial repair and fixation system products continued to increase. In the future, it will focus on technological innovation as the core driving force, providing higher-performance products and professional services that better meet clinical needs, contributing to the high-quality development of China's medical health industry.